Protective Clothing Market

Protective Clothing Market Share & Trends Analysis Report, By Material Type (Polyethylene, Polypropylene, Polyester, Tyvek, Others) By Application (Biological Safety, Chemical Protection, Cleanroom Protocols, General Laboratory Use, Infection Control) By End-User (Pharmaceutical Companies, Biotechnology Firms, Research & Academic Laboratories, Clinical and Diagnostic Laboratories, Contract Research Organizations (CROs) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

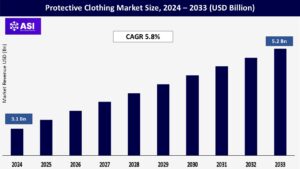

CAGR: 5.8%

Last Updated : February 3, 2026

The global protective clothing market size for the Life Sciences Industry was valued at approximately USD 3.1 billion in 2024 and is projected to reach USD 5.2 billion by 2033, growing at a CAGR of 5.8% during the forecast period (2025–2033).

In the life sciences sector, protective clothing is needed for safety, contamination control, and regulatory compliance, including in pharmaceutical manufacturing, biotechnology labs, research entities, and clinical laboratories. These include lab coats, coveralls, gloves, gowns, and hoods that act as barriers to chemical, biological, and particulate hazards. In cleanroom and biosafety environments, the demand for sterile, disposable, and multi-layer materials is significant.

The reasons for the forecasted growth in protective wear across the life science space are driving growth, including the growth of the pharmaceuticals and biotechnology businesses, increased R&D around infectious diseases and biologics, and global regulatory requirements on workplace safety and product purity. In addition, the recent increase in restrictions and infection control protocols from COVID-19 to combat the spread of infectious diseases and the increase in zoonotic diseases worldwide has collectively accelerated protective clothing market growth within life sciences.

The global increase in pharmaceutical and biotechnology production, particularly in the aftermath of COVID-19, has also led to an increase in the demand for protective clothing to maintain sterile environments and to help keep manufacturing free from contamination. Infection control has not only become paramount for patient safety but also for keeping the product drug intact.

The protective garments, such as sterile coveralls, gowns, gloves, and masks, have now become a regulatory requirement under cleanrooms and biosafety level (BSL) facility operations. According to the International Federation of Pharmaceutical Manufacturers & Associations (IFPMA), global pharmaceutical research and development (R&D) investment surpassed USD 230 billion in 2023, with enormous funding having been provided for vaccines, oncology, and biologics, where controlled and sterile environments are paramount.

Large pharmaceutical companies such as Pfizer and Moderna invested heavily in their manufacturing capacity for mRNA platforms, which has also meant applying rigorous biosafety protocols, along with a substantial amount of sterile protective wear in their production and quality control labs.

Plus, regulatory agencies, including the U.S. FDA, EMA, and WHO, also require stringent adherence to Good Manufacturing Practices (GMP), which involves a host of contamination control factors that require wearing approved personal protective clothing. These regulatory pressures continue to support sustained protective clothing market growth, where there is high turnover in production-specific hoods and PPE (personal protective equipment).

As a response to infectious risks such as COVID-19, Mpox (Monkeypox), and recent zoonotic spillover threats (e.g., avian influenza H5N1), there is a heightened focus on laboratory biosafety and worker protection. Any laboratory working on pathogens at the BSL-3 and BSL-4 level must have sophisticated personal protective clothing including impermeable suits, respirators, and multiple-glove systems to prevent transmission, contamination, and accidental exposure.

According to the Global Health Security Index (2023), over seventy countries have committed to increasing investment in ‘high containment’ facilities for the treatment and surveillance of high-risk pathogens for infectious disease surveillance and outbreak preparedness.

For example, India’s National Institute of Virology (NIV) and Germany’s Robert Koch Institute have expanded BSL-3/4 laboratories to support a rapidly expanding portfolio of infectious agents requiring high containment handling, driving demand for high-quality protective apparel, including Tyvek suits with sealed covers for gowns, and full-body sealed coveralls. These developments reflect ongoing innovation within the protective clothing industry.

Manufacturers are developing advances in material design and contaminants such as microporous laminates as well as SMS fabrics to meet performance expectations while providing comfort. This growth is increasingly evident in regions where public health threats meet global R&D progress in virology, bacteriology, and vaccine development, therefore adding strength to the global protective clothing market for life sciences.

High costs of specialized protective garments are one of the major limitations to the growth of the protective clothing market in the life sciences space, especially for cleanroom and high-containment laboratory applications. Because many of the specialized garments are made from Tyvek, microporous laminates, multi-layered SMS fabric, etc., they utilize complex manufacturing methods, require fabrication processes that ensure sterility, and must meet strict standards such as ISO 14644, EN 14126, ASTM F1670/F1671.

These types of garments are more than double the cost of normal protective clothing, thus posing a barrier to use in a cost-conscious world. This challenge is especially acute in developing countries and academic research institutions that are often short on budgets. A 2023 report from UNESCO found more than 50% of biomedical research institutions in low-and middle-income countries (LMICs) identified “insufficient funding for safety equipment” as a critical barrier to appropriately utilizing PPE. Disposable protective clothing also has an ongoing cost, especially in high-turnover laboratories.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Material Type |

Polyethylene Polypropylene Polyester Tyvek Others |

| By Application |

Biological Safety Chemical Protection Cleanroom Protocols General Laboratory Use Infection Control |

| By End User |

Pharmaceutical Companies Biotechnology Firms Research & Academic Laboratories Clinical and Diagnostic Laboratories Contract Research Organizations (CROs) |

| Key Players |

DuPont 3M Company Ansell Limited Lakeland Industries, Inc. Kimberly-Clark Corporation Honeywell International Inc. Alpha Pro Tech, Ltd. Lakeland Global Medline Industries, Inc. Cardinal Health, Inc. |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Protective Clothing Market for the Life Sciences Industry is segmented by material type and end-user. By Application, Each segment plays a critical role in enhancing safety, minimizing contamination, and ensuring compliance with regulatory standards in life sciences environments, providing a clearer understanding of the protective clothing market size across key applications

Tyvek will have the largest market share in 2024, given its superior barrier performance to most particles, aerosols, and low-level liquid chemicals. This product (or suitable equivalent materials) is common in cleanrooms for pharmaceutical purposes, sterile environments, and biosafety labs because of its breathable and durable qualities. Polypropylene is gaining traction in disposable lab coats, coveralls, and caps, primarily in academic labs and low-risk areas.

It is cost-effective and easy to dispose of in high-turnover environments. Polyethylene likewise has excellent chemical-resistant properties and is commonly used in laboratories where corrosive materials are handled. The SMS (Spunbond-Meltblown-Spunbond) material segment is rapidly growing due to its combination of protection, comfort, and breathability, especially as it relates to longer duration wear in research and pharmaceutical production settings.

Pharmaceutical companies led the protective clothing market, accounting for the largest protective clothing market share in 2024. The contribution of pharmaceutical companies stems from extensive regulatory oversight, particularly from the FDA and EMA, surrounding contamination control and protection from workplace exposure (potentially) during the manufacturing and quality assurance phases of the drug production.

In the biotechnology market, the advanced protective clothing is being rapidly embraced, especially in genetic engineering and bioprocessing studies, where the risk of contamination must be minimised. Additionally, research and academic laboratories continue to contribute to the market due to the increasing volume of studies involving infectious diseases and molecular biology.

Disposable and sterile protective clothing is important in clinical and diagnostic laboratories that rely on handling accurate samples, alongside protecting their staff from biohazards. Also, Contract Research Organizations (CROs) are investing in premium protective clothing as they undertake outsourced research and clinical trial work across a range of therapeutic areas.

In 2024, Infection Control will hold the largest share of the market due to the need to minimize the transmission of pathogens in pharmaceutical, biotech, and clinical settings. The COVID-19 pandemic highlighted high-quality protective garments, and the elevated level of awareness around infection risk will continue the trend for protective garments such as gowns, gloves, and coveralls.

Facilities focused on vaccine development, microbiology, and virology utilize large volumes of infection control clothing in order to help sustain BSL protection levels. Cleanroom protocols represent a growing segment, particularly in sterile pharmaceutical and biopharmaceutical manufacture.

Protective clothing associated with cleanrooms (coveralls, boot covers, hoods, etc.) is designed to protect against contamination from particles and fibers. The increasing use of biologics and cell and gene therapies will drive demand for ISO-compliant cleanroom clothing. Biological safety applications are becoming more prevalent as research progresses on infectious diseases, genetic engineering, and immunotherapy.

Protective garments and other forms of high-protection clothing are critical tools in biosafety cabinets and high-containment laboratories (BSL-3 and BSL-4). Finally, there is chemical protection for laboratories and manufacturing areas where hazardous or corrosive agents are handled. With the increasing complexities of pharmaceutical synthesis and quality testing methods, the demand for chemical-resistant suits, aprons, and gloves will only continue to grow.

The general laboratory, however, covers a full spectrum of routine academic and clinical research tasks. Lab coats, scrubs, and disposable aprons typically sold in this category are routinely used in lower-risk settings with high activity levels, such as teaching hospitals or university laboratories. Although this segment represents a smaller share, the large base provides continued demand.

In 2024, North America holds the largest market share at 38.9%, making it the leading contributor to the global protective clothing market size. Due to its substantial pharmaceutical and biotechnology industries, very strong regulations, and substantial market penetration of advanced protective clothing. The US is a significant player with strong investment opportunities in cleanroom technologies and infectious disease research, contributing significantly to the overall protective clothing market size at the global level.

Tight market and regulatory landscapes are exemplified by key pharmaceutical regions of Massachusetts, California, and Ontario (Canada), with a high frequency of BSL-3/4 laboratories and large-scale manufacturers that require sterile and high-performing appropriate protective apparel. Further, U.S. OSHA and CDC guidelines elevate the importance of stringent site safety protocols.

Europe embodies a large market with the prospect for significant growth driven by countries such as Germany, France, UK, Switzerland, and Netherland. Europe benefits from a significant life sciences research ecosystem with high levels of clinical trial activities and strong worker protection regulations established under the European PPE Regulation (EU) 2016/425.

Cleanroom and contamination control standards instituted for GMP-certified pharmaceutical sites in Europe have further elevated the need for disposable ISO compliant protective clothing. Aging structures in Western Europe, coupled with increased R&D in biotechnology, will allow for steady market growth.

The Asia-Pacific market is expected to grow with the fastest CAGR of 7.6%, from 2025 to 2033. The rapid expansion of pharmaceutical manufacturing and related supply components, increasing government investments in healthcare infrastructure, and rising domestic biotechnology companies are driving volume and value in Asian countries such as China, India, Japan, and South Korea.

Examples of major growth enablers include India’s website “Pharma Vision 2030” plan and China’s expanding vaccine production capacity. Our understanding of clinical research outsourcing and an increase in focus on pandemic availability have promoted the adoption of protective clothing across all research labs and manufacturing units in the Asia -Pacific region.

Latin America and the Middle East & Africa are expected to have moderate growth driven by increased funding and investment in pharmaceutical infrastructure and public health research. Countries like Brazil, Mexico, South Africa, and the United Arab Emirates are working toward building regional manufacturing capacity and enhancing their biosafety readiness, and demanding protective garments.

However, the slow rate of adoption in Latin America and the Middle East & Africa remains rooted in systemic issues such as limited healthcare budgets, high levels of import dependencies, and inequitable access to safety equipment. Nevertheless, international collaborative partnerships and capacity building will assist in improving penetration within these regions over time.

The market was valued at USD 3.1 billion in 2024.

The market is projected to grow at a CAGR of 5.8% from 2025 to 2033.

The Tyvek material hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include DuPont, 3M Company and Ansell Limited.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 The Protective Clothing Market, By Material Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 The Protective Clothing Market, By Application

5.3 The Protective Clothing Market, By End User

6.1 North America The Protective Clothing Market, By Country Type

6.1.1 The Protective Clothing Market, By Material Type

6.1.2 The Protective Clothing Market, By Application

6.1.3 The Protective Clothing Market, By End User

6.2 U.S.

6.2.1 The Protective Clothing Market, By Material Type

6.2.2 The Protective Clothing Market, By Application

6.2.3 The Protective Clothing Market, By End-User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping