Skin Imaging Systems Market

Skin Imaging Systems Market Share and Trend Analysis, By Technology (2D Imaging Systems, 3D Imaging Systems, Digital Dermatoscopes, Confocal & Multiphoton Microscopes, AI-Enabled Software Platforms), By Application (Skin Cancer Diagnosis, Cosmetic & Aesthetic Evaluation, Teledermatology, Dermatology Research, Other Clinical Applications), By End User (Hospitals & Multispecialty Clinics, Specialized Dermatology Clinics, Research Institutes & Academics, Beauty Salons & Aesthetic Centers, Home-Use & Consumer Devices) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 8.4%

Last Updated : April 2, 2026

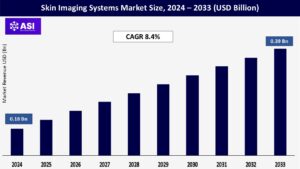

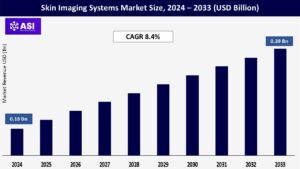

The global skin imaging systems market size was valued at USD 0.18 billion in 2024 and is projected to reach USD 0.39 billion by 2033, expanding at a compound annual growth rate CAGR of 8.4% during the forecast period (2025–2033).

Skin imaging devices are becoming inevitable in clinics. We use handheld dermatoscopes routinely for magnified surface images of lesions and moles, usually photographing them digitally. Otherwise, whole-body scanners (2D and newer 3D ones) scan a patient’s skin entirely.

That is essential for monitoring many moles over several years, being able to catch subtle changes early on. For internal layers, confocal microscopes provide cellular-scale imaging non-surgically, but they’re more specialized. The true value lies in early detection. Detecting melanomas or virulent SCCs when they are small makes a huge difference.

We also apply these systems extensively to inflammatory disorders – measuring acne severity or monitoring psoriasis plaque response to therapy more objectively than subjective scoring. Images are tangible proof for patients and insurers alike. Cosmetic practices rely on them as well.

VISIA-type complexion analyzers uncover UV damage and pore faults not visible to the naked eye, influencing laser or peel treatment plans. Serial imaging after the procedure demonstrates effectiveness, balancing patient expectations.

Telehealth integration is revolutionary. We take dermoscopic images in-house, securely upload them into the EHR, and receive remote specialist reads quickly, particularly valuable for rural patients. As hardware becomes smaller and software more intelligent (automating measurements, alerting on changes), they reduce workflows and increase patient trust with visual evidence.

Patient numbers with alarming lesions or long-term inflammatory diseases are rising dramatically due to cumulative UV insult, increased longevity, and increased public education regarding the health of skin. This heavily overloads dermatology offices. Precocious detection of melanoma, which is crucial for survival, requires sophisticated imaging modalities, pushing them from discretionary to mandatory.

Today’s digital dermatoscopes allow accurate longitudinal follow-up of suspicious lesions through serial imaging, enabling accurate year-to-year measurement and comparison to detect minimal changes undetectable to the naked eye. High-risk patient full-body mapping is increasingly popular.

Although significant, AI’s predominant current clinical application is triage assistance – the classification of lesions that require immediate specialist examination from high volumes of images. Evidence suggests the ability to decrease unnecessary biopsies by 30% or more in certain environments.

Since biopsies are costly, require resources, and generate anxiety, imaging with algorithms safely excluding malignancy brings significant gains in efficiency. Changing guidelines supporting routine imaging surveillance further fuel demand beyond specialist centers into wider practice.

The aesthetic dermatology segment utilizing skin imaging technology is growing at lightning speed, driven by increasing disposable income, social media-fueled beauty standards, and the popularity of non-surgical procedures (lasers, injectables, peels). Patient expectations have changed; they expect advanced, technology-enabled consultations, not only procedures.

Imaging is at the core of this. Equipment such as multi-spectral complexion analyzers utilizes UV or polarized light to make subclinical skin injury (incipient sun spots, vascular problems, pore topography) visually apparent that would normally be unseen.

This, in effect, shows treatment need and individualizes treatment plans. After treatment, quantitative imaging objectively demonstrates effectiveness. Presenting clients with quantifiable proof of results (e.g., diminished wrinkle depth, decreased hyperpigmentation months afterward) greatly improves credibility, builds loyalty, and generates repeat business.

Practices leverage this objective documentation to justify premium pricing. Medical aesthetics has been a motivating factor for even non-medical beauty salons to invest in genuine imaging technology.

Furthermore, the spread of consumer-level, phone-synced home devices, though not clinically accurate, continues to keep consumers interested in skin analysis and frequently directs consumers towards professional care. As imaging technology continues to evolve in measuring subtle gains in texture and laxity, its strategic value in this profitable market is likely to increase further.

The main barrier to widespread utilization of advanced skin imaging systems is still the high initial capital outlay. The exorbitant price of full-service scanners and advanced dermatoscopes is a great financial stumbling block, especially for smaller practices, free-standing clinics, and institutions running within tight budgets in many parts of the world.

Working against this issue is the poor reimbursement structures. Payers, such as insurers and government healthcare programs, often deny coverage for the imaging tests themselves, especially the related analysis elements. Coverage is mostly defaulted to standard visual inspection and biopsies.

Reimbursement routes for standard imaging-based monitoring continue to be unclear, with uneven use of available procedural codes and payment levels commonly considered less than the cost of the technology. Thus, practices are presented with unsustainable options: take unaffordable losses that reduce margins, shift costs to patients (developing access disparities), or not adopt at all.

Lengthy regulatory certification procedures also increase development costs. Until that time, predictably priced models of reimbursement are in place, adoption will continue to be focused mainly in large institutional environments and high-end cosmetic businesses. That limitation prevents wider access to important diagnostic innovation for patients and obstructs more comprehensive clinical use.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

2D Imaging Systems 3D Imaging Systems Digital Dermatoscopes Confocal & Multiphoton Microscopes AI-Enabled Software Platforms |

| By Application |

Skin Cancer Diagnosis Cosmetic & Aesthetic Evaluation Teledermatology Dermatology Research Other Clinical Applications |

| By End User |

Hospitals & Multispecialty Clinics Specialized Dermatology Clinics Research Institutes & Academics Beauty Salons & Aesthetic Centers Home-Use & Consumer Devices |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Two-dimensional imaging systems are the conventional technological basis in the dermatological imaging industry. Marked by their conventional digital cameras and dermatoscopes, these products reign supreme owing to their ease of use, affordability, and proven track record in day-to-day clinical practice.

They deliver high-resolution surface imaging adequate for initial evaluations, documentation, and teledermatology consults. But three-dimensional imaging platforms are seeing fast-moving adoption, especially for whole-body anatomical mapping and longitudinal surveillance applications.

Using structured light or stereophotogrammetry, these devices produce high-resolution topographical reconstructions, allowing for accurate volumetric measurement of lesions and allowing clinicians to identify subtle morphological alterations consistent with the progression of malignancy.

Confocal reflectance microscopes and multiphoton imaging systems are in a niche category, providing non-invasive, cellular-resolution visualization of skin anatomy. This modality is useful for sophisticated diagnostic protocols and research studies, complementing or replacing histopathological examination in certain situations.

On all modalities, the incorporation of artificial intelligence for automated image segmentation, feature annotation, and risk stratification is on the rise. These analytic advancements greatly speed diagnostic workflows and enhance clinician decision-making confidence.

Although continuous miniaturization and cost-cutting moves will expand the availability of advanced technologies to a wider audience, two-dimensional imaging is expected to command substantial market share, especially in cost-constrained settings and initial screening protocols, because of its inherent usefulness and simplicity of implementation.

Diagnosis of skin cancer continues to be the leading application segment, fueled by international public health efforts focused on early detection and the highly significant prognostic value of early melanoma identification. Imaging systems are widely used for detailed lesion documentation, comparative serial analysis, and the delineation of essential diagnostic features like asymmetry, border irregularity, and color variegation.

Cosmetic and aesthetic dermatology represents a significant and fast-growing field of application. Imaging technologies are a requirement in this setting for pretreatment evaluation—measuring baseline parameters such as pigmentation irregularities, vascular appearance, and textural features to individualize interventions like laser treatments, energy-based devices, and topical treatments.

Post-procedure imaging offers objective measurement of therapeutic effectiveness, with the ability to improve patient communication and satisfaction. Teledermatology is a key growth area, with strong impetus provided by the need for off-site delivery of care.

Smartphone-adapted dermatoscopes and cloud-based image handling platforms enable specialist consultation over geographical distances, with enhanced access in underserved areas. Dermatological research is an important niche, utilizing high-resolution technologies such as confocal microscopy to explore pathophysiologic mechanisms at the subcellular level, guiding new therapeutic development.

Other clinical applications acquiring momentum involve quantitative scar evaluation, objective measurement of hair follicle health and density, and standardized monitoring of wound healing progress. Synergy between advanced imaging hardware and sophisticated analytical software continually increases the value proposition in all these areas of application.

Hospitals and large medical centers are the big spenders. These require flexible imaging solutions. Hospitals and multispecialty clinics form the dominant end-user segment. These facilities normally acquire a diversified array of imaging technologies to support specialized departments such as dermatology, oncology, plastic surgery, and wound care centers.

Interoperability with hospital information systems and electronic health records are top-of-mind purchasing factor. Specialized dermatology clinics are another key target market, with a high-volume patient population.

These practices value operational effectiveness, which stresses resilient, mid-range imaging systems, specifically high-end digital dermatoscopes for everyday exams and lesion monitoring, designed to fit high-speed clinical practices and also promote patient interaction through visual confirmation.

Academic research centers and specialized labs constitute a separate segment centered on innovation. These organizations invest mainly in research-grade, high-resolution imaging systems, including confocal and multiphoton microscopes, to carry out translational research studying disease mechanisms, validating new imaging biomarkers, and evaluating novel therapeutic interventions.

The aesthetic medicine industry, medical spas, and cosmetic dermatology clinics are increasingly using easy-to-use imaging devices that are intended for patient interaction.

They are used for the purpose of treatment planning and display outcomes visually, thereby directly affecting service marketing and customer retention. Lastly, the home-use segment is a nascent category, stimulated by consumer-available smartphone attachments and mobile apps fostering self-monitoring.

Although this segment creates new market dynamics, uptake is hindered by considerations over clinical validation and embedding within professional care pathways. Buying decisions among all end-user groups are ultimately determined by weighing technological capability, total cost of ownership, workflow consistency, and the particular clinical or commercial goals the technology supports.

North America leads the market, supported by advanced healthcare infrastructure, policies for reimbursement favorable to diagnostic imaging, and early and widespread adoption of digital health technologies.

The United States drives leading demand, driven by well-established population-level skin cancer screening programs and substantial private and public sector investment in AI-based diagnostic technologies. Canada shows consistent growth through provincial telehealth initiatives and dermatology access schemes.

Mexico’s market growth, though from a lower base, is spurred by private aesthetic clinics in urban areas adopting imaging for cosmetic treatments and growing middle-class demand for preventive skin check-ups.

Europe is a large, mature market, with Germany, France, and the United Kingdom being major contributors. Strict regulation guarantees high-quality devices and stringent safety standards. Public health policies that are favorable to preventative dermatological care, such as regular screenings, spur adoption.

Growth is also boosted by concerted European telehealth initiatives improving cross-border specialist accessibility and increased consumer spending on minimally invasive cosmetic procedures, especially in Western and Southern European countries. Harmonization initiatives make market access easier, although reimbursement differs by country.

The Asia Pacific region is predicted to have the highest growth rate in the world. This is driven by fast-growing healthcare spending, a growing middle class with increasing disposable income for cosmetic procedures, and greater public awareness about skin cancer and overall dermatological well-being, particularly in China, India, Japan, and Southeast Asia.

Government initiatives to expand access to healthcare in rural areas, combined with the accelerated spread of telemedicine platforms that leverage standard imaging devices, are tremendously driving regional adoption of skin imaging technologies in varied environments.

LAMEA is an emerging, high-growth market region, though from a relatively low base today. Drivers are key urban hubs in Brazil, Mexico, Saudi Arabia, the UAE, and South Africa that fuel demand through investments in private healthcare facilities and increasing specialty dermatology services to meet the needs of high-income populations and medical tourism.

Increased awareness of aesthetic treatments also fuels adoption. Nevertheless, substantial market growth is moderated by limited reimbursement systems for diagnostic imaging, and ongoing gaps in healthcare infrastructure confining access in rural and underserved areas throughout these regions.

The global Skin Imaging Systems Market was valued at USD 0.18 billion in 2024.

The market is projected to grow at a CAGR of 8.4 % from 2025 to 2033.

The 2D segment holds the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include FotoFinder Systems GmbH, Canfield Scientific, PIE Medical Imaging, Quantificare, DermLite, SIAscope (Demed), EvoluDerm Technologies

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Skin Imaging Systems Market, By Technology

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Skin Imaging Systems Market, By Application

5.3 Skin Imaging Systems Market, By End User

6.1 North America Skin Imaging Systems Market, By Country

6.1.1 Skin Imaging Systems Market, By Technology

6.1.2 Skin Imaging Systems Market, By Application

6.1.3 Skin Imaging Systems Market, By End User

6.2 U.S.

6.2.1 Skin Imaging Systems Market, By Technology

6.2.2 Skin Imaging Systems Market, By Application

6.2.3 Skin Imaging Systems Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping