Trauma Fixation Devices Market

Trauma Fixation Devices Market Share and Trend Analysis, By Technology (Internal Fixation, External Fixation), By Application (Long-Bone Fractures, Periarticular Fractures, Pelvic and Acetabular Fractures, Pediatric Fractures, Spinal Trauma, Open and Comminuted Fractures), By End User (Hospitals, Ambulatory Surgical Centers, Outpatient Clinics, Academic & Research Institutions, Rehabilitation and Long-Term Care Facilities) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

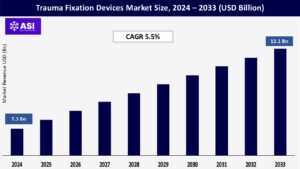

CAGR: 5.5%

Last Updated : March 31, 2026

The global Trauma Fixation Devices Market size was valued at USD 7.3 billion in 2024 and is projected to reach USD 12.1 billion by 2033, expanding at a compound annual growth rate CAGR of 5.5 % during the forecast period (2025 – 2033).

Trauma fixation devices refer to a number of instruments—plates, screws, rods, nails, and external fixators—that are utilized to stabilize fractures and reconstruct bone integrity following traumatic injury. These products are used in all orthopaedic trauma care facilities, such as emergency departments, operation theaters, and outpatients.

Internal fixation techniques (e.g., intramedullary nails, locking plates) are popular for long-bone fractures, while external fixators are used in complicated open fractures or polytrauma cases. Increases in road traffic accidents, sports injuries, falls, and elderly populations susceptible to osteoporosis fuel demand.

Moreover, technological innovations—like anatomically shaped plates, bioresorbable screws, and minimally invasive fixation implants—improve patient outcomes and shortens recovery time. Developing economies are investing in orthopaedic infrastructure, thus providing increased access to sophisticated fixation technologies.

With healthcare providers focusing on early mobilization and reduced hospital stays, trauma fixation devices have become an important part of complete fracture management protocols, enabling bone union, minimizing complications, and maximizing functional recovery.

Worldwide, the number of bone fractures due to road traffic accidents, sports injury, workplace injuries, and falls among geriatrics has seen a substantial rise in the last decade. In developing countries, rapid urbanization and poor road safety have led to an explosion of high-energy traumas.

Long-bone fractures (tibia, humerus, femur) account for nearly 30 % of total orthopaedic admissions according to hospital registries, requiring internal or external fixation for re-establishing skeletal stability. In addition to this, the elderly are at risk of low-energy falls and osteoporosis-induced fractures around the hip and spine, which need surgical treatment.

As hospitals acknowledge the significance of early surgical management to decrease morbidity and health expenditures, usage of locking plates, intramedullary nails, and modular external fixators has increased dramatically.

As trauma registries become larger and knowledge of fracture management best practices increases, orthopaedic surgeons increasingly turn to contemporary fixation devices that provide biomechanical benefits, e.g., angular stability and load-sharing design over more conventional means such as casting or traction. This trend, alongside government efforts to enhance trauma care networks, still fuels market growth.

Advances in imaging, materials science, and surgical methods have spurred the evolution of trauma fixation devices toward minimally invasive, more anatomically consistent, and patient-specific solutions. The use of titanium alloy plates with pre-contoured geometries enables fracture fixation with minimal disruption of soft tissues, decreased perioperative blood loss, and decreased risk of infection.

Computer-assisted pre-operative planning software and intraoperative navigation systems facilitate accurate screw placement and plate positioning. Bioresorbable fixation materials (e.g., poly-L-lactic acid composites) have become available for specific pediatric and craniofacial conditions to obviate the need for removal of implants.

Furthermore, locking compression plates (LCP) integrate angular stability with dynamic compression ability for the advantage of comminuted or osteoporotic fractures. Minimally invasive percutaneous plating methods, under the guidance of fluoroscopy or 3D imaging, reduce operative time and hasten the mobilization of patients.

At the same time, robotics-assisted orthopaedic surgery is beginning early clinical adoption with enhanced accuracy in implant placement. As manufacturers spend money on research and development to add sensors and intelligent coatings that identify early infection indicators or track load distribution, the market is likely to turn towards “intelligent” fixation solutions. These technological advances are improving surgeon preference, broadening indications, and eventually increasing revenue growth.

While superior clinical outcomes, these high-tech trauma fixation devices are frequently expensive, with a notable price premium over standard implants. Pre-contoured anatomically shaped parts and specialized locking plates may be two to three times as costly as simple stainless-steel alternatives.

Across most low- and middle-income nations, strained healthcare budgets and restrictive reimbursement policies discourage high-volume use of premium implants. Insurers can limit reimbursement to standard plates and screws, requiring surgeons and hospitals to weigh patient outcome against cost.

Patient out-of-pocket expenses can be excessively high, deferring surgical treatment or the adoption of less-than-ideal implants. Furthermore, public health system procurement policies tend to aim at cost reduction at the expense of device innovation, limiting vendor bargaining power and the introduction of newer technologies.

Exorbitant import duties on medical devices in certain countries also add to costs. Consequently, fewer expensive, branded fixation solutions are used by some smaller clinics and hospitals despite their inferior long-term effects and extended rehabilitation periods.

Unless cost gaps narrow through local production, increased supply-chain effectiveness, or beneficial reforms in reimbursement levels, price sensitivity and variable insurance coverage will continue to pose major growth obstacles in certain markets.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

Internal Fixation External Fixation |

| By Application |

Long-Bone Fractures (Femur, Tibia, Humerus) Periarticular Fractures (Distal Femur, Proximal Tibia, Distal Radius) Pelvic and Acetabular Fractures Pediatric Fractures Spinal Trauma (Pedicle Screw Systems) Open and Comminuted Fractures (Staged Fixation) |

| By End Use |

Hospitals Ambulatory Surgical Centers (ASCs) Outpatient Clinics Academic & Research Institutions Rehabilitation and Long-Term Care Facilities |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The trauma fixation devices market is segmented into internal fixation and external fixation technologies at a broad level. Internal fixation comprises intramedullary nails, plating systems (locking plates, dynamic compression plates), screws, and wires. Intramedullary nails, frequently employed for femoral, tibial, and humeral shaft fractures, exhibit load-sharing features and facilitate early weight-bearing.

Plating systems, particularly locking compression plates, ensure angular stability and are used in periarticular and osteoporotic fractures. Screws (cancellous, cortical) and cerclage wires are used in fragment stabilization in small bones or comminuted fractures. Niche but increasingly used bioresorbable fixation materials are also being used in pediatric trauma and craniofacial cases.

In contrast, external fixation technologies, unilateral, bilateral, circular ring fixators, are utilized in open fractures, polytrauma cases, and limb lengthening surgeries. The newer developments include modular hybrid fixators that integrate ring and monolateral elements, allowing multiplanar fixation.

External systems also include patient-friendly components such as quick-release clamps and struts that can be adjusted, facilitating slow correction of deformities. Minimally invasive percutaneous application is still a mainstay of both internal and external procedures, and continuing advances in navigation and intraoperative imaging further ensure accurate placement of implants.

The applications of trauma fixation devices depend on the location and severity of the fracture. Long-bone fractures—femur, tibia, humerus—are most common, and need either locking intramedullary nails or plating systems. Femoral fractures usually use cephalomedullary nails for intertrochanteric fractures, and tibial shaft fractures can be treated with reamed or unreamed intramedullary rods.

Periarticular fractures—distal femur, proximal tibia, distal radius—are dependent on anatomically shaped locking plates for conforming to joint geometry and restoration of the articular surface. Pelvic and acetabular fractures use specialized recon plates and screws that follow complex anatomical corridors.

Simple wrist or ankle fractures can employ mini-plates and cannulated screws for minimal invasion. Fractures in children usually demand flexible intramedullary nails or bioresorbable implants to prevent growth plate interference.

Polytrauma and open fractures, more so Gustilo Grade II/III, demand staged treatment, with initial external fixator application for temporary stabilization followed by definitive internal fixation after the improvement of soft-tissue status. Also, some vertebral compression fractures include percutaneous pedicle fixation screws, extending the trauma fixation portfolio into spinal use.

Hospitals are the main end users of trauma fixation devices, holding the highest market share because of the availability of advanced surgical infrastructure, specialized orthopaedic trauma teams, and intensive care units. Inside hospitals, specialty trauma centers, and tertiary care institutions spur high-volume implant use.

Outpatient clinics and Ambulatory Surgical Centers (ASCs) are becoming popular for minimally invasive fracture fixation, facilitating cost control and shorter hospital stays; yet these facilities see only a narrow set of low-risk cases.

Specialty orthopaedic ambulances or mobile surgical units in rural areas increasingly employ portable external fixation units for emergency stabilization, but contribute marginally. Academic and research hospitals invest in clinical studies and training courses, affecting technology uptake by demonstrating new fixation methods.

Rehabilitation hospitals and extended care facilities indirectly make use of fixation devices in revision operations or restorative procedures. Government-owned public hospitals, particularly in growing economies, hold market shares in volume acquisitions with their bulk procurement policies, though private chains of hospitals take premium segments with tailored device solutions.

As insurance coverage increases internationally, patient interest in private hospitals with access to cutting-edge implants is increasing, further influencing end-user distribution patterns.

North America maintains a leading position, fueled by strong healthcare spending, sophisticated trauma care facilities, and well-established reimbursement structures that support innovative implants. The United States leads the market due to well-established trauma registries, high adoption of minimally invasive therapies, and early FDA approvals.

Growing elderly population and healthy lifestyle of the baby boomers are contributing to fracture rates, with private-public collaborations financing research into new plates and nails. Canada’s single-payer system provides uniform access, with controls on cost potentially slowing the implementation of high-end technologies.

Europe represents the second-largest proportion, backed by government programs to improve trauma services and elderly populations in Western nations. Germany, France, and the UK make significant investments in orthopaedic research, with an early adoption of locking plate systems and bioresorbable materials.

Eastern European markets are developing as a result of increasing hospital infrastructure and rising per capita expenditure on healthcare. Strict regulatory approvals (CE marking) and national procurement tenders focus on cost-effectiveness, thus affecting device prices and constraining the immediate adoption of new implants in some countries.

The Asia Pacific market is ready to experience strong growth due to the strongly advancing healthcare infrastructure in China, India, and Southeast Asia. Increased orthopedic trauma cases due to industrialisation, vehicular accidents, and sports injuries fuel demand for fixation devices.

Domestic manufacturers increasingly partner with multinational companies through joint ventures to develop cost-competitive implants, catering to price-sensitive markets.

Government subsidies and insurance programs in countries such as China and Japan increase access to higher-level trauma care. Challenges present are unequal rural access, regulatory differences, and differences in training among surgeons between countries.

Latin America and the Middle East & Africa together constitute a changing market environment with low existing demand but high growth prospects. In Latin America, Mexico and Brazil are at the forefront of investing in trauma centres, albeit against adoption hurdles provided by economic volatility and reimbursement shortfalls.

In the Middle East, GCC nations ramp up expenditure on healthcare in orthopaedics, importing premium fixation devices from the US and Europe. Africa’s urban centres experience incremental infrastructural development while rural areas lag. Home-based manufacturing and non-governmental organisation (NGO) activities strive to fill accessibility gaps during the forecast period.

The global Trauma Fixation Devices market was valued at USD 7.3 billion in 2024.

The market is projected to grow at a CAGR of 5.5 % from 2025 to 2033.

Internal Fixation hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include NuVasive Inc., Orthofix Medical Inc., Conmed Corporation, B. Braun Melsungen AG, Hindustan Syringes & Medical Devices, Baumer S.A., Wright Medical Group

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Trauma Fixation Devices Market, By Technology

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Trauma Fixation Devices Market, By Application

5.3 Trauma Fixation Devices Market, By End User

6.1 North America Trauma Fixation Devices Market, By Country

6.1.1 Trauma Fixation Devices Market, By Technology

6.1.2 Trauma Fixation Devices Market, By Application

6.1.3 Trauma Fixation Devices Market, By End User

6.2 U.S.

6.2.1 Trauma Fixation Devices Market, By Technology

6.2.2 Trauma Fixation Devices Market, By Application

6.2.3 Trauma Fixation Devices Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping